Tax Planning for Salaried Individuals: A Comprehensive Guide

Basic plan for saving of tax for Salaried Individuals, Understanding of Tax Structure, Basic Rule of Saving, Investment Ideas

FINANCE BLOGS

CA Rajkumar Patel

5/24/20244 min read

Understanding Taxation on Salary Income

Salary Structure: Taxation on salary income is a pivotal aspect of financial planning for salaried individuals. The salary received by an individual comprises several components, each with distinct tax implications. The primary component is the basic pay, which forms the foundational part of the salary and is fully taxable. Allowances, such as house rent allowance (HRA), leave travel allowance (LTA), and special allowances, are provided to meet specific expenses and may be partially or fully exempt from tax under certain conditions.

Perquisites, commonly referred to as perks, are benefits provided by the employer in addition to the salary. Examples include company-provided accommodation, cars, and stock options. These perks are usually taxable and are added to the salary income to determine the total taxable income.

The taxable income is calculated by aggregating all the components of the salary and subtracting eligible exemptions and deductions.

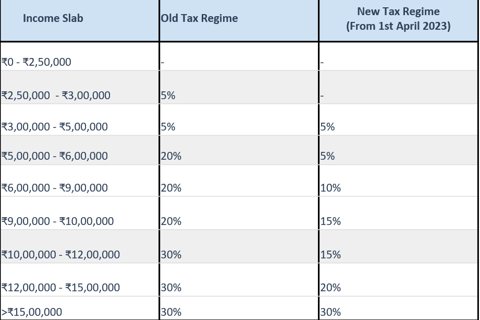

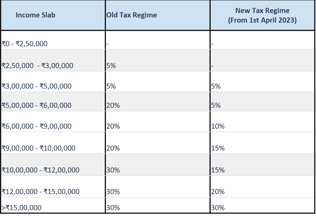

Income tax slabs and rates are then applied to this taxable income to compute the tax liability. The income tax slabs for salaried individuals are progressive, meaning the rate of tax increases with the increase in income. For instance, In the Old Tax Regime, the tax rate for income up to INR 2.5 lakh is nil, while income above INR 2.5 lakh and up to INR 5 lakh is taxed at 5%, and so on, with higher rates for higher income brackets. Check in the below table slab rates for both tax regimes.

Tax Deducted at Source (TDS) plays a crucial role in the taxation of salary income. Employers are required to deduct TDS from the salary before disbursing it to the employee. The TDS is calculated based on the estimated taxable income and the applicable tax slabs. This mechanism ensures that tax is collected at the source of income, thereby reducing the burden of lump-sum tax payments at the end of the financial year.

Understanding the implications of various salary components on overall tax liability is essential for effective tax planning. For instance, optimizing the structure of allowances and perquisites can lead to significant tax savings. Therefore, a thorough knowledge of how salary income is taxed can empower salaried individuals to make informed decisions and plan their finances efficiently.

Deductions and Tax Assessment for Salary Income

Tax planning for salaried individuals involves understanding and leveraging various deductions available under the Income Tax Act.

One of the primary sections offering substantial tax relief is Section 80C, which allows deductions for investments in instruments like Public Provident Fund (PPF), Employees' Provident Fund (EPF), National Savings Certificate (NSC), and more, up to a limit of ₹1.5 lakh per annum.

Additionally, Section 80D provides deductions for health insurance premiums paid for self, spouse, and dependent children, with an upper limit of ₹25,000, and an additional ₹50,000 for senior citizen parents.

Other relevant sections include Section 80E, which permits deductions on the interest paid on education loans, and

Section 80G, covers donations to specified charitable institutions. These deductions play a crucial role in reducing taxable income, thus lowering the overall tax liability.

The process of tax assessment for salary income begins with the filing of income tax returns (ITR).

Form 16, provided by the employer, is essential as it summarizes the salary paid and the tax deducted at source (TDS). To calculate the taxable income, one must start with the gross salary and subtract allowable exemptions such as House Rent Allowance (HRA), Leave Travel Allowance (LTA), and the standard deduction. Following this, eligible deductions under various sections are applied to arrive at the net taxable income.

Effective tax planning strategies include optimizing the salary structure by incorporating tax-efficient components such as meal vouchers, telephone reimbursements, and conveyance allowances. Additionally, making full use of the income-saving rule, which encourages investments in tax-saving instruments early in the financial year, can significantly minimize tax liability. By strategically planning investments and expenses, salaried individuals can ensure maximum tax benefits.

Practical examples, such as a case study of an individual utilizing Section 80C and 80D deductions, can illustrate the impact of these strategies on reducing taxable income. Such examples highlight the importance of being proactive in tax planning to achieve financial efficiency and compliance.

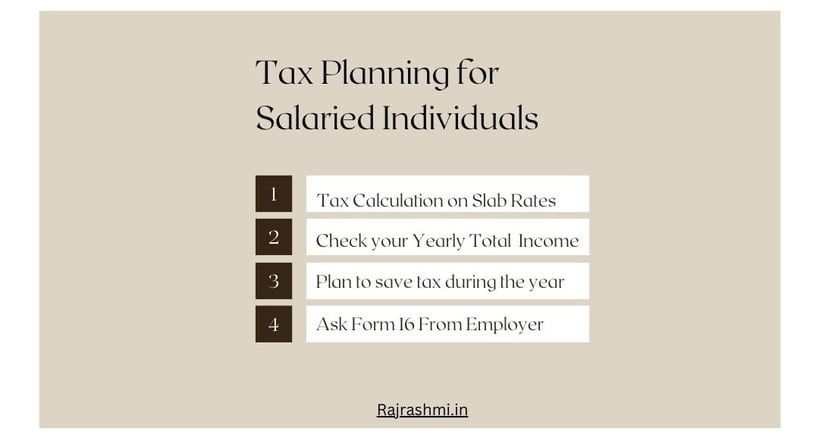

Tax Planning for the year:

For any salaried individual, whose income is under higher Slab Rates, TDS shall be deducted by his employer from his monthly income. Employees do not understand how the tax is calculated on their income and how to plan for the tax savings. Here are some ideas to save your money.

Step 1: Calculate your total income for the Financial year and check whether it is above the non-taxable income Slab. You have to understand income tax slabs in taxation. If yes, then you get how much amount you need to plan for tax savings.

Step 2: Make investments and get your health insurance for the Deductions from your total income. For these, You can take the help of Chartered Accountants.

Step 3: Provide all investments and insurance-related details or documents to your employer, so that he can calculate the proper tax for the deduction.

Step 4: After the year-end, ask your employer for Form 16 which provides you with the salary income details with your investment details submitted to the employer. Form 16 helps you get the details of Tax Deducted by your employer from your income.

Welcome

carajkumarpatel@gmail.com